Are Federal Student Loans Even “Loans”? From leniency to forgiveness to taxpayer spending. Fairer: allow bankruptcy

The educational-industrial complex is laughing to the bank.

By Wolf Richter for WOLF STREET.

One person’s loan is another person’s property. If the loan is cancelled, the asset is destroyed. That’s the way it is.

No one pays anymore on federally-backed student loans, after two years of perpetual forbearance, countless campaign promises of forgiveness, various targeted forgiveness programs already in place, and now, the big thing, the universal forgiveness program being yanked out.

Total outstanding student loans, assuming they are still “loans” at all, remained at $1.59 trillion in the second quarter compared to the first quarter, according to the New York Fed’s Household Debt and Credit Report. They have been relatively stable since the first quarter of 2020 as new loans were added while virtually no one made payments and as the numerous forgiveness programs eat into the balance sheet from the other side.

Federal student loans.

Federal student loans account for about $1.3 trillion of the $1.59 trillion total in student loans, according to a separate report from the New York Fed. The rest are Family Federal Education Loans (FFEL) owned by commercial banks and private loans.

It’s the $1.3 trillion in federal loans that were all shifted into perpetual forbearance in Spring 2020 and are now up for forgiveness.

The median federal student loan balance is $18,773 — meaning half of federal student loan balances are less than $18,773 and half are more.

The outliers that everyone is talking about, the $150,000 and $200,000 loan balances, were accumulated by a small percentage of borrowers who have legal, medical, etc. forgiveness at all.

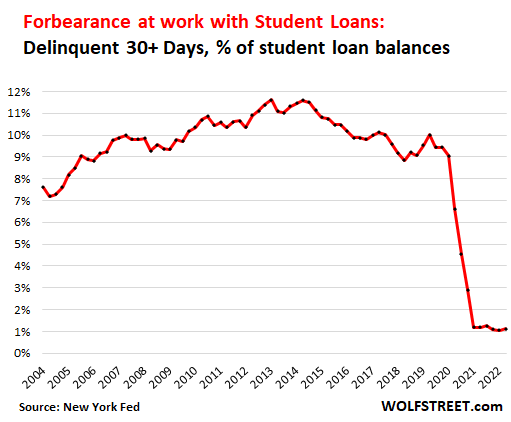

Forever-tobearance “solved” late payments.

The amount of student loans that were 30 days or more past due fell to just 1% from the official 9.4% of total balances before the pandemic.

The default rate for federal student loans is 0%. All were automatically placed in forbearance programs in Spring 2020, which have been renewed time and time again and are still in effect. When a loan is placed on deferral, it is classified as “ongoing” rather than “overdue” regardless of payment status.

FEEL and private student loans not included in forbearance programs accounted for all delinquent loans.

Student Loan Waiver and Termination.

In addition to the list of existing student loan forgiveness programs — government loan forgiveness, teacher loan forgiveness, closed school release, and others — there is now forgiveness when students feel the education-industrial complex screwed them up .

Just Thursday, a federal judge granted preliminary approval to a settlement that would cancel $6 billion in student loans from over 200,000 students who claimed they were cheated at 153 mostly for-profit colleges.

Few of these schools have been held accountable. So it’s the taxpayers who will pay the $6 billion, not the education industrial complex that has received the $6 billion over the years and poked fun at the bank.

Most importantly, a general forgiveness program is being worked out by the administration. The proposal began with $10,000 forgiveness per borrower. But this taxpayer stinginess leaves many voters deeply frustrated, and anger boils over, pressuring politicians to buy more votes or buy the same votes again by increasing the forgiveness amount to $50,000, perhaps with income caps.

Next, auto loan forgiveness… just kidding, kinda.

The median transaction price for new vehicles is nearly $46,000, and the median selling price for used vehicles is $28,000.

In comparison, the median federally supported student loan is $18,773. Just another consumer loan. Paying $200 a month for 10 years isn’t the end of the world – and 10 years of wage increases and inflation will ease that burden.

And if people can’t even make a $200 payment, they can’t make a $400 payment or an $800 payment on a car loan either. So when do we buy votes with the promise of car loan forgiveness?

It’s unfair that people who bought a car because they have to drive to work should be forced to pay back these loans. We need universal car loan forgiveness. The government could simply buy up all outstanding auto loans and then forgive them up to $50,000 each, perhaps with some income caps, like $250,000 per person and $500,000 per married couple filing jointly.

Think of it this way: it would be a huge boost to the economy because instead of making car payments, those people could then spend their money on other things.

It’s not fair, but fairness has nothing to do with it.

The government (taxpayers) financed these student loans by borrowing in the government bond market. It then passed this borrowed money through the students to the educational-industrial complex, expecting most of the money plus interest to be repaid by the borrowers after they started work. Her payments would have helped the government service the debt it incurred to fund student loans. But that’s over. In the future, the taxpayer will pay off the borrower’s loan.

In other words, the waiter who would have liked to go to college but couldn’t afford it now has to pay off the student loans of software engineers who went to college. It’s not fair, but fairness has nothing to do with it. This is about buying votes. And they hope that the waiter can’t find out.

Let the bankruptcy courts decide what will be discharged and how much borrowers have to pay each month.

Borrowers cannot currently redeem their student loans in the bankruptcy court system. But they found something much more attractive to get rid of their debts: politicians who want to buy votes with someone else’s money, namely taxpayers’ money.

But that doesn’t have to be the case. The same politicians could change the law to allow for student loan redemptions in bankruptcy courts.

So it would be a judge deciding how much this programmer with a degree from Stanford can pay each month for the next 10 years and how much this teacher with a degree from OSU can pay each month. And the judge can then waive the rest that cannot be paid. This is how personal bankruptcy has worked since the Bankruptcy Reform Act of 2005. When filing personal bankruptcy, people can’t just walk away from all their debt.

Student loan borrowers would then consider going through with it and making the payments; or file for bankruptcy, get the blemish on your credit report, get forgiveness on student loans if you have any, and make payments by court order for many years to come.

This system already exists for private bankruptcies. It’s not perfect, but it’s functional. And it would relieve borrowers who really can’t pay. And it would be a lot fairer for everyone around, including the waiter who couldn’t afford to go to college and doesn’t really want to pay off the student loans other people got to graduate.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally understand why – but do you want to support the site? You can donate. I appreciate it very much. Click on the Beer & Iced Tea Mug to learn how:

Would you like to be notified by email when WOLF STREET publishes a new article? Sign up here.

![]()

Comments are closed.